Leasing Vs. Buying A Car

Posted on January 18, 2021

One of the most common questions in the purchasing process is whether it is better to lease or purchase a vehicle.

One of the most common questions in the purchasing process is whether it is better to lease or purchase a vehicle.

There are pros and cons to both leasing and buying methods so the answer for you will depend on how long you intend to own the vehicle, and how you plan to use it.

In A Nutshell

Generally speaking, if you intend to keep the vehicle for a long time (5+ years) or drive more than 20,000 kms/year, then financing might be more appropriate for you. Financing will enable you to pay off the vehicle so you can keep driving, debt-free, and monthly-payment-free for years and you can finance an extended warranty to better match your use and length of ownership.

However, if you like the idea of driving a new car for 2 to 5 years (i.e. while it has its factory warranty in effect), and you drive less than 20,000 kms/year, or if you like driving a more expensive vehicle for a lower monthly payment, then leasing could be a great option for you.

Why Lease a Car?

One of the biggest perks of leasing is that you always have a new vehicle can make a great impression, no matter if you're going to a work appointment or are just out having fun.

Thanks to the lower costs of leasing, shoppers can often afford a better vehicle. They can go for the more luxurious or performance-packed model/trim level than they might have otherwise chosen. That means having a car that's loaded with all of the latest features and technologies, which can make every trip so much more enjoyable.

Of course, there's a limit to how many miles you can drive each year as part of the lease agreement, but the car is covered by the factory warranty, so you don't have to worry about paying for virtually any repairs. By returning the vehicle at the lease end date, you also avoid taking on the big, expensive problems that crop up as cars age.

Instead of having to pay taxes for the entire vehicle up front, shoppers who choose to lease pay less. They're only responsible for taxes on the portion of the car they use, which means more savings.

How Car Loans Work

When you finance a car you are taking out a loan for the full purchase price of the vehicle plus HST. Each repayment you make is comprised of interest and principal to amortize the loan to $0 over the term of the loan. Once the accumulated principal repayments exceed the depreciation on the vehicle (usually occurs around the 4-5 year mark) you are "in equity" on the vehicle. Any time after that, should you sell or trade in your vehicle, you can regain your equity. If you trade it back in, you receive value for the HST on your trade value. If you sell it, you do not.

How Car Leases Work

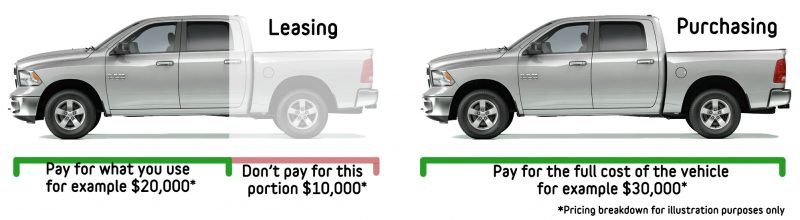

In contrast, lease payments are very different. In a lease, it is the pre-HST purchase price of the vehicle amortized to the vehicle's depreciated value at the end of the lease term (known as its residual value), that determines the lease amount financed. As the vehicle's depreciated value is not zero at the end of the lease term, you in effect only pay for what you use of the vehicle. You also only pay HST on your monthly payments, so you do not pay to finance the HST on the portion of the vehicle you have not used.

For these two reasons, in a lease your monthly payments will be lower than under financing for the term of the lease. In an open-ended lease, you are responsible for the vehicle being worth at least what its residual value is and/or you may use any excess equity towards a future purchase.

In a closed-ended lease you may simply turn the vehicle in at the end of the lease, however there is never any equity at lease end with this type of lease. Under either lease, you may also choose to keep the vehicle past its maturity date by either buying out the lease or arranging either a lease that amortizes to zero or alternate financing.

What to Be Careful of When Leasing a Vehicle

You need to be aware that the lease terms can vary between dealerships, so read through them carefully (i.e. 36 is not equal to 39 months). This can greatly affect how good of a deal you're really getting when it comes to leasing any vehicle.

You need to be aware that the lease terms can vary between dealerships, so read through them carefully (i.e. 36 is not equal to 39 months). This can greatly affect how good of a deal you're really getting when it comes to leasing any vehicle.

Also, make it a point to note the actual price you agree to pay for the car, plus the interest rate for the lease.

Always verify if the lease is open-ended (you may just turn the vehicle in and walk away) or closed-ended (you are responsible for the residual value). If it's an open-ended agreement, you need to pay attention to the portion of the agreement that talks about wrapping up the lease. With either option, you need to be aware of any penalties related to driving excess kilometers, plus wear-and-tear on the vehicle so you know exactly what you're getting into.

Leasing Incentives

To make leasing an even better option for shoppers, FCA Canada has started offering several compelling incentives. If you're in the market for a new car, truck or SUV, this is a great way to get that vehicle you always dreamed of driving every day. Ask our Finance Specialists what's available today and get car financing pre-approval from CarHub.

Visit our experts at CarHub to learn more about the deal.